Housing without debt

Our flawed housing economy, and what we can do about it.

If you haven’t seen Adam McKay’s film ‘The Big Short’ yet, do. It paints — in clever, funny, depressing human detail — the perfect corruption of the financial system in the years leading up to the sub-prime mortgage collapse. The crisis before the crash.

It is now more or less universally accepted that there is something fundamentally wrong with our housing economy. Not just the centralised industrial production models we use to produce housing: our dependence on a few large development companies to buy the land, beat their way through local community resistance, and build rows of poor quality, unsustainable mass-housing that fewer and fewer of us can afford. The Big Short is not about those industrial housing models. It’s about the economy behind them.

And we obviously need to understand it. Because housing is one of the basic platforms upon which our social and economic prosperity are built, and yet the systems we use to provide it are failing.

It’s not just the UK that faces this dilemma. Almost every developed economy is now facing some version of the same crisis. It is a failure of truly global proportions, a fundamental flaw in our economic model, arguably destroying any reasonable hope for sustainable, equitable urban development in the 21st century; and there seems to be nothing governments can do to ‘fix’ it with the tools currently available to them.

The simplistic story of the housing crisis is that we have a shortage of homes. ‘Build more homes’, the argument goes, ‘and prices will go down’. Unfortunately it’s not that simple. When you drill down a bit further you realise that the housing crisis is really much more to do with land. Land is a finite commodity — at least, land with planning permission, close to jobs is. As Mark Twain said “Buy land, they don’t make it anymore.”

Except, he wasn’t quite right either. We actually make land all the time. Only about 2–3% of the landmass of the UK is built-upon, because most land doesnt have planning permission. We (citizens, represented by our local governments) can ‘create’ land through the planning system by giving our consent for new land to be reclassified for residential use. The problem is that communities — not surprisingly — don’t want to release new land for housing, because they’re the ones who bear all the costs of poor quality, unsustainable, overpriced development, but get none of the benefits. And no developer — no matter how much land they have— will ever build homes so quickly that prices stop rising.

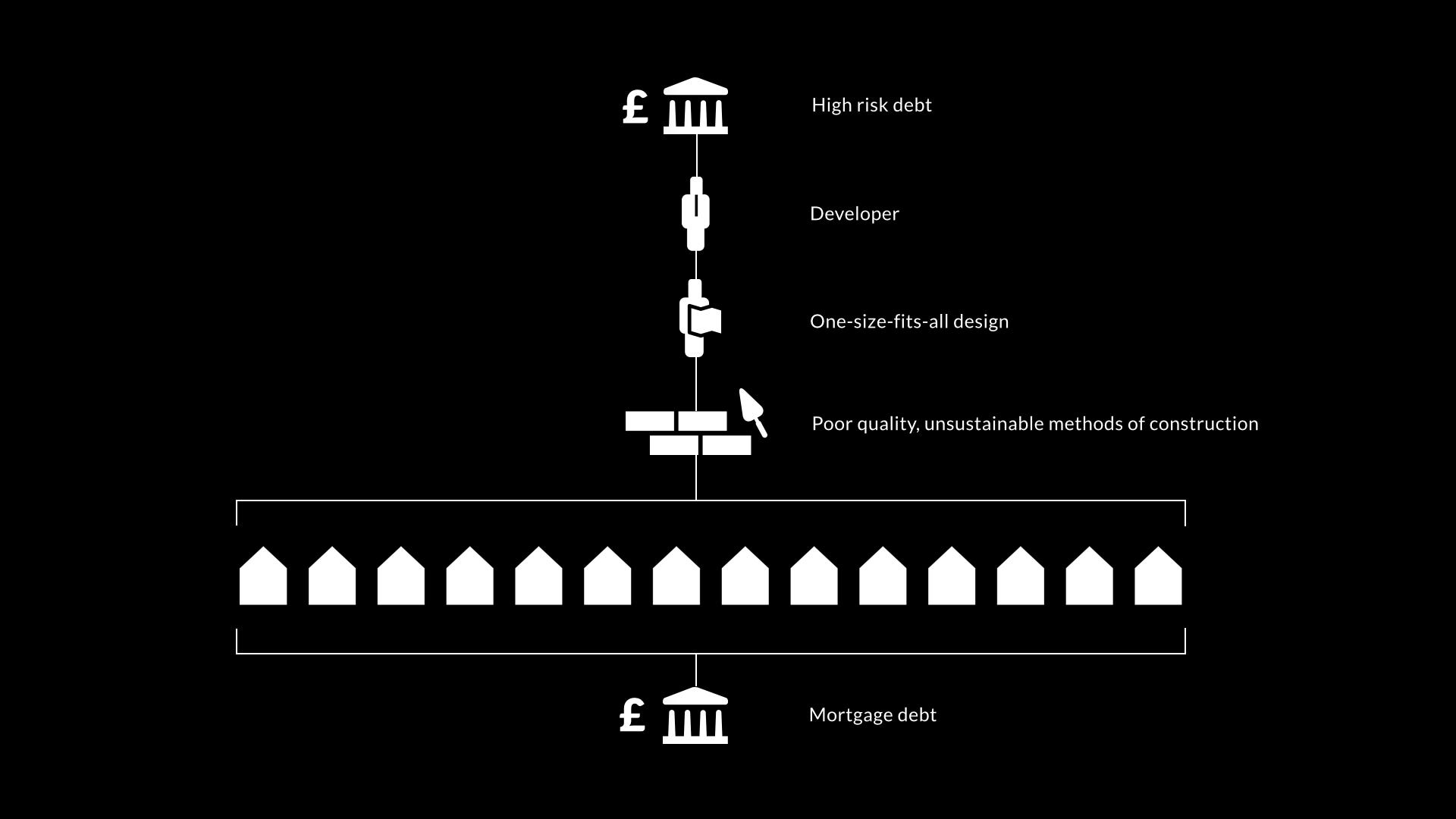

So in a way, even land is not the real market. Land scarcity is just the baseline economic condition within which the real market emerges. That market is not selling us the land itself, but the means of access to that land: debt. We will all, always, need somewhere to live, so as long as the number of homes is finite, then the amount of debt can be infinite. When it comes to selling mortgages we are, quite literally, a captive market.

Housing market = debt market

So when we talk about the housing market, we should understand that what are being sold are not so much the homes as the mortgages — homes are just the vehicle. In the middle class, we tell ourselves that if we rent our homes, we’re poor, and if we own our homes, we’re rich. But even those who technically ‘own’ their homes are still renting the capital that they bought it with. The painful realisation is that ultimately all of us are just renting money (debt) down the chain from the private companies that create that money in the form of loans. The main difference between us is that the rich can rent money at a very low rate of interest, the middle class at another rate, whilst the poor can only rent it at Wonga rates. This allows us all to feel like we are richer than someone else, whilst actually just servicing bigger and bigger debts.

Once everyone is fully locked into this closed housing system, it can then be fed with debt from both ends. At the top, the big land developers rely on debt finance to buy the land, fight through the planning system and build properties (at great risk). At the bottom, citizens then take on ever higher mortgage loans to be able to afford those properties (at great risk). As prices inflate, so do the loans, and as the loans inflate, so do the prices, and so do the risks. These loans can be bundled as mortgage-backed securities, traded, labelled double or triple-A, but ultimately, at some point, this whole system stops working. Because maths. When it does, ironically, governments then have to take on even more debt trying to subsidise the whole system and rebuild it.

It is important to understand that even after 2008, that is still the economy that shapes our housing systems and our cities, and it comes at a catastrophic cost.

The first cost is a social cost, and we all experience it at some point in our daily lives — in term of our mental and physical health, social isolation, inequality, long commutes, life in tiny, poor quality, unsustainable homes, high heating bills, loneliness, and years spent working in bad jobs to pay off vast mortgages. For the large part, the homes we live in were not designed to improve our lives, they were designed to be property assets which we happened to end up living in.

The second cost is the instability of this market — made evident in 2007/08. Since that crash, house prices have re-escalated to unprecedented levels — to such a degree that it is almost impossible to imagine the cycle will not repeat itself**.

The third cost is simply that it leaves most people behind. On small sites, or sites outside growing metropolitan areas, or for those on low-incomes, speculative development is simply ‘not viable’ (that’s to say, it’s not sufficiently profitable for investors to bother).

The final cost is a purely economic one. Inflating house prices might look like growth on paper, but of course, the reality is that they are burying the real economy under a mountain of debt. As Lord Adair Turner argues, the more money we ossify into balance-sheet property values, the less cash is moving around the real economy, being productive. The housing crisis exposes as false the traditional political association between capitalism and ‘free markets’. In fact, today, capitalism is eating the market. More specifically, the market for housing debt is sucking the life from all the other markets for actual things (products and services).

Where does the money you pay for a new home go?

What most people don’t realise is just how much of the money we pay for our homes is not going into the production of that home at all but simply to meet the debt, developer profits or the inflated value of locked-out land.

So where does the money go? For an example, let’s take a typical new house on the outskirts of London, one that costs £250,000 to buy.

Of the £250,000 sale price, only a relatively small amount actually goes into building the home itself. In fact, the developer’s aim is to spend as little money as possible on the home — to reduce its size and quality as far as they can. Even if a technological innovation allows the developer to build a home for less, they will still sell the house for the same price (whatever the market will allow), and just take a larger margin. This was illustrated by the absurd story of New Labour’s flagship ‘£60K homes’, which cost £200K+ to buy, no less than any other home.

Even that £250,000 is not the true full cost of the home to us. A mortgage of perhaps £212,000 paid at 4% over 25 years adds an additional shadow cost of £125,000 in loan interest. That borrowing cost alone is larger than the build cost of the home.

In other words, building homes — even really good, high-performance ones– is actually pretty cheap. What is crippling us is the cost of access to this spiralling debt economy around housing, which creates scarcity, and therefore inflation, therefore speculation, therefore monopoly, and therefore further scarcity. (There’s a superb explanation of how this works here, written by the New Economics Foundation)

So how do you solve a problem like housing?

This leaves governments in zugzwang — all moves lose. Let prices keep inflating, and the majority will find themselves priced-out of a home. Let prices crash, and millions of middle class people risk being thrown into negative equity. Deregulate the market and all you get is worse houses for the same price (and even more alienated communities). Regulate the market and risk freezing up the whole thing altogether. Lose, or lose. Sink, or sink.

But what if, instead of trying to tweak or repair the doomed, debt-driven housing market, governments were to adopt a different, slightly more oblique strategy: build a lifeboat.

Rather than trying to resolve the problem by regulating or deregulating the existing market, what if we could create a whole new, separate, parallel market for housing, which runs on a fundamentally different economic operating system, and yet can exist alongside the existing one; acting almost like a slow-release valve.

A parallel housebuilding industry

What would that market be, and how would it break our dependence on debt? First, it would change who builds our homes. It would be founded on the most obvious piece of common sense that has yet to be applied in policy: that the only people who will always build the best, most sustainable, most healthy, most affordable homes they can are the people who are going to live in them and pay the heating bills: us. The economic logic is pretty simple: when we buy the land and procure homes for ourselves, we are not building them primarily as speculative financial assets to sell or rent, but as things to use, and we want the best home we can have for as little money as possible.

The strange thing is that once you have the opportunity to act as your own developer (whether it’s as an individual or as a group), the same house on the same plot of land instantly can become as much as 1/3 cheaper; simply because you are no longer paying a developer (and their shareholders) to take on all the unnecessary risk of fighting through the planning process, borrowing and marketing the home to you. Furthermore, there’s no reason to pay an ‘Affordable Housing’ (Section 106) contribution, because the housing can actually be affordable in the first place for people on most incomes (more on that later).

But you should still pay a ‘Community Infrastructure Levy’ (CIL) — a cash contribution to the local council to invest in the new roads, schools, and community facilities that you’re going to use while you’re living there. So already the total cost of your home has come down from £250,000 to £185,000.

This up-front capital cost can be reduced even further if you can do some of the work for yourself, or, instead of building the whole house up-front, start with a smaller more basic house, and grow it over the years that you live there. In effect, it’s lowering your dependence on short-term, top-down financial capital by allowing you to invest long-term, bottom-up human capital.

Perhaps that might get our initial cost down to £155,000.

The digital citizen sector

That bit is not new. It has always been better, cheaper, more sociable and more sustainable when people procure their own homes. But ‘self-build’ and ‘custom-build’ development has always been regarded as too difficult, too diverse, too unpredictable, impossible to scale, too tough to regulate. But that no longer needs to be true.

If there’s one lesson we can take from digital & web platforms over the last two decades, it is that it is now possible for networks of small, distributed producers to outperform large, centralised, one-size-fits all industrial models. Think YouTube, Wikipedia, AirBnB. The mission of the WikiHouse project is to help do something similar for the design and production of housing, to allow high-performance customised homes to be designed and produced locally by a distributed network of small companies for the same cost as mass-produced home. In the 21st century, we are no longer stuck with the false choice between the state and the market, the public sector and the private sector. The citizen sector now needs to be recognised as a viable, scaleable industrial force.

What does this mean for us as homeowners? Put simply, it means that with access to land, a bit of digital infrastructure*, and a distributed marketplace of architects, manufacturers, project managers and builders, the process of developing a beautiful, high performance customised home could actually be significantly easier, more affordable and more enjoyable than buying a house that already exists.

A parallel market for land

However, that still leaves us with the problem of the inflated price of the land itself. One option might be simply to lease (rather than sell) plots of land to homeowners. This requires no up-front capital, so you could sign a long lease on the plot, and all you need to do is build your home for £50k and move in. For most people, housing affordability is a problem of capital, not earnings, so this could work — but the ground rental price could still be prohibitively high in high-value areas.

But what if we were to go further, and create a parallel market for land too, based on the same very simple rule: that the land can only be bought, owned and developed by the people who are going to live there? In other words, what if we were to separate the speculative property market (investors seeking to use houses primarily as inflation or rental assets), from the market of people who just want a place to live. It’s still a market, and you still can buy and sell your home when you want to move house, but the market price would be driven not by what speculative investors can afford to pay, but by what other local families can afford to pay. So in the same way that the value of a piece of agricultural land is less than a piece of land with planning permission for homes (say, £20,000 per hectare compared to £6m per hectare), in many areas the value of the same piece of land in this parallel land market would be less than it would be in the mainstream market; perhaps something like £3m per hectare.

That could bring the total cost of our £250,000 home down to something more like £105,000.

But wait.

- How do you distinguish between speculative and personal land use?Actually, the UK tax system already makes this legal distinction, and so did the Self & Custom building Act. So it turns out this bit isn’t that hard.

- What mechanism would we use to create this parallel market? On the immediate term, there are lots of ways this could be ‘hacked’ without law reform. Community Land Trusts, for example are — in a way — already a kind of parallel land market. It might be possible to create a kind of ‘National Land Trust’ or ‘National Land coop’ which actively owns all such sites and sub leases the plots on its own terms. Equally, local authorities can commit to selling sites they own directly to custom and self-builders only. However a much more scaleable approach would be to just hard-code it into planning law itself by creating a new land use class, C5 ‘Dwellings procured and owned by their occupants’ as a distinct land market. Essentially giving planners the power to designate custom-build zones. A question frequently raised by some planners is, ‘is that really a different use of land?’ The answer is yes. In the 20th century, planning was simpler. Different uses of land looked different. A factory looked different from a shop, and so on. But to be able to fulfil its core function of setting a regulatory framework for the market, planning today needs to have a smarter understanding of ‘use’ in the economy. Although they may both superficially look like houses, in real economic terms, ‘using land to make a thing to sell or rent’ and ‘using land to make a place for yourself to live’ are completely different products; as different as a hot meal is from a hedge fund.

- Why would landowners opt-in to this parallel market if its going to reduce the value of the land? There are a few possible reasons why existing home and landowners might choose to change their land from C3 to C5, perhaps for tax benefits, to ensure long-term affordability, or perhaps to achieve higher quality, more resilient neighbourhoods over the long term or simply to be less exposed to volatile market fluctuations. In some rare cases, local authorities might even use it to force speculators who are sitting on large areas of land — refusing to develop it — to sell sites to those who will build (a more sophisticated version of ‘use it or lose it’). However, most land classified under C5 would be new land — that’s to say land which was previously assigned an agricultural or industrial use. This is powerful for two reasons. The first is that it gives local councils (and perhaps more importantly, local communities) the power to say ‘we don’t want this kind of development, but we do want that kind of development.’ Research by Shelter, YouGov and others has shown that contrary to popular belief, we are not a nation of NIMBYs, we’re just not easily fooled. Support for new development dramatically increases if local residents can be sure that new development will be high quality, sustainable, and will benefit them, their families and their community rather than speculative developers. Local families might even be offered a first right of refusal on new plots in their area. In other words, C5 is powerful because it recognises that the way out of the deadlock is not less, but more democracy. It can unlock land for development that our current housing economy can’t. The second reason this is powerful is that C5 can be applied through ‘land auctions’ . The basic idea of land auctions is rooted in a core principle of the planning system, which is that the ‘planning gain’ (the increase in land value that is created when land is given planning permission for homes — almost £6m per hectare in our previous example) should be recaptured and invested for the common good. Instead of the current ‘Section 106’ model, which attempts to claw some of this back from developers after development as a form of negotiated tax on unaffordable homes, land auctions allow councils to (in effect) buy the land cheaply before granting planning permission and then sell it off with planning permission, keeping the entire difference. This allows councils and local communities to just… keep the land affordable in the first place. Any planning gain that is captured (say, £2.5m per hectare) can then be used to pay for new schools or infrastructure voted for by the local community, or invested into affordable plot and community support programmes, helping disadvantaged families access the same opportunities as middle class ones.

All this might seem strange and unfamiliar to those accustomed to our rather complicated, compromised and arguably corrupted existing housing systems, but it is in many ways a much more straightforward model.

The key message is this: there is still a way that we can build genuinely affordable and sustainable homes in the 21st century, and it doesn’t even require public funding.

A parallel finance market

Within our parallel market, the total price of our typical home is now down to £105,000, most of which is going into build cost. But that’s still more than many people can afford to buy outright with their savings —most will probably need some kind of loan. Let’s say £85,000.

So we need a final layer to our parallel economy: a form of lending which is based not on private banks conjuring new debt into existence, but by loans based on re-investing savings. In other words, we’re probably talking about something like a revival of the mutual building society; only this time it’s digital, and distributed. There are others far more qualified to talk about this challenge — and an exploding field of peer-to-peer micro-loan platforms which are looking at how to distribute risk and cut out the big banks. However, it seems reasonable to assume that, minus the volatility of the speculative land and mortgage market, and with households’ repayments making up a much smaller percentage of their overall income, this parallel housing market is likely to be a reassuringly safe, boring form of finance. Less Big Short, more It’s a Wonderful Life.

In 25 years, our family can fully own their home for a borrowing cost of only £50,000, and that money can be recycled to help the next generation build. With monthly payments of £449 or less, they can spend their additional money on extending their home or… just living. As Danny Squires of Spacecraft, (developing WikiHouse in New Zealand) puts it: ‘Which would you prefer: a house worth £145,000 more on paper, or an extra £220,000 cash to spend over the next 25 years?’

All of this can happen on the same piece of land we started with at the beginning - equivalent to somewhere on the outskirts of London. But the same equation can apply anywhere, with no upper density limit that individuals or groups (known in Germany as ‘baugruppen’) can develop at.

The case for a new housing strategy

To be clear, this is not a utopian pipe dream. It is already beginning to happen. It works. Neither does it require aggressive reform of the existing banking and housing systems.

As you step out of the cinema after watching The Big Short, it’s hard not to feel dumbstruck and despondent — realising that nothing short of a huge, radical political revolution will change the banking system, or the housing market, even though almost all of us are agreed that they are failed systems.

But we don’t need to. As housing analyst Yolande Barnes of Savills explains very lucidly, the one thing we can rely on the speculative housebuilding sector to do is… to keep doing more or less the same thing it has always done: build a limited number of homes and sell them for as much as it can. And that’s fine. We don’t need it to stop it doing that. But we do need to stop being totally dependent on it. It will never, ever build enough homes. There is a missing sector in housing. In the 19th century it was the philanthropic sector. In the 2oth century it was the public sector. In the 21st century it will be the citizen sector, a huge, distributed, well-regulated economy of small builders, with its own production capacity, its own land supply, even its own financial institutions.

If this experiment fails, then we will have lost nothing. But if it succeeds, we will have done something much more than just solving our affordability crisis. We will have prototyped an economy that knows how to invest in housing as a platform for our social and economic success rather than our failure. We will have created a whole new distributed, circular housebuilding industry, building local production capacity, and a competitive, innovative construction market that will get really, really good at building sustainable homes, before exporting those solutions to an urbanising world. We will also have set a precedent for a more democratic, more inclusive, more organic, more resilient form of urban development, something done-by, not done-to citizens.

So not a Big Short, but a Very Small Long — one with the potential to deliver immeasurably huge returns for everyone.

*We are currently bringing together a consortium of partners to build the first version of this digital infrastructure for housing production. If you’d like to find out more, join us or support us, please do get in touch.

** As experts such as Miles Gibson of CBRE will explain, a crucial difference between 2016 and 2006 is that this time around, much of the price inflation is backed not by debt (sub-prime mortgages to poor people) but by equity (the super-wealthy parking their money in property portfolios). This doesn’t mean the housing market won’t crash, it just means fewer banks will go bust when it does. In theory.